Kenya and Uganda are stepping up efforts to gain greater control over their oil and mineral industries, signalling a broader East African push to stop exporting raw materials only to buy back finished products at far higher prices.

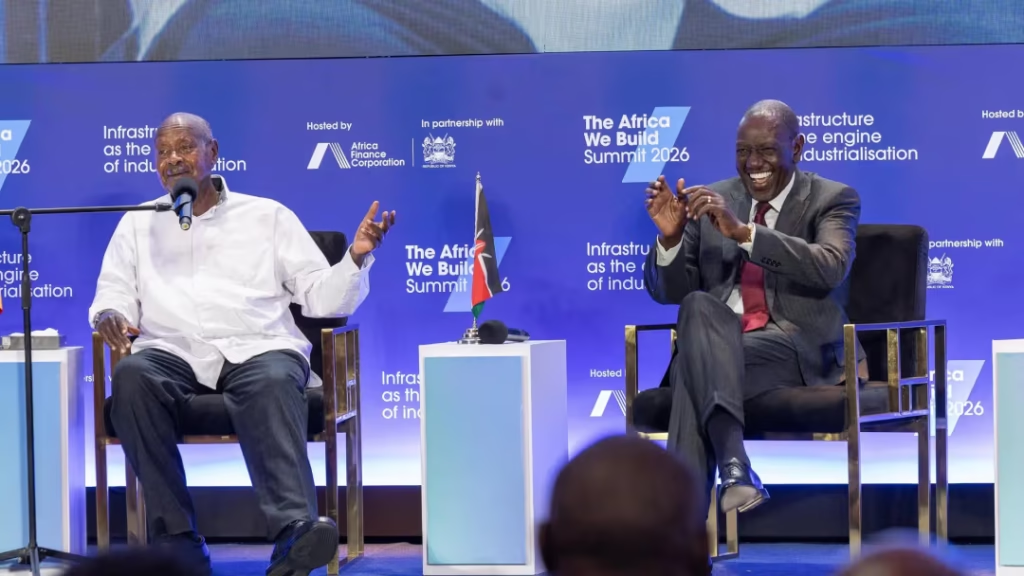

Speaking during the 2026 “Africa We Build” Summit in Nairobi, President William Ruto revealed that Kenya plans to invest in Uganda’s proposed 60,000-barrel-per-day oil refinery. The move follows Uganda’s interest in acquiring a stake in the Kenya Pipeline Company and reflects a growing spirit of regional cooperation in the energy sector.

The announcement came shortly after businessman Aliko Dangote unveiled plans for a 650,000-barrel-per-day refinery in Tanga, Tanzania, expected to be completed within the next four to five years. Together, the projects point to a deliberate regional shift from dependence on imported petroleum products towards locally refined fuel backed by African ownership.

Ruto said Kenya’s investment in Uganda’s refinery was part of a shared vision for managing East Africa’s natural resources collectively and more profitably.

Ugandan President Yoweri Museveni criticised the long-standing practice of exporting raw minerals cheaply while foreign companies reap massive profits from processing them abroad. He cited an example where Ugandan iron ore was purchased at just US$45 per tonne before being resold internationally for as much as US$900 per tonne despite the ore’s high purity.

Museveni argued that exporting unprocessed minerals effectively exports employment opportunities as well. He made a similar case for gold, noting that processed gold commands nearly three times the value of raw exports.

Ruto broadened the discussion to include minerals essential for the green energy transition, such as cobalt, lithium, copper, and rare earth elements. He said Africa must work together to position itself competitively within global green manufacturing industries instead of remaining merely a supplier of raw inputs.

Drawing comparisons with the European Coal and Steel Community, which later evolved into the European Union, Ruto suggested that regional resource integration could strengthen not just economies but long-term political and industrial unity across Africa.

Also Read: Man Killed in Arrow Attack During Land Adjudication Event in Narok

He also acknowledged tensions that have occasionally slowed cooperation between African states. Referring to a previous disagreement over iron ore processing between Kenya and Uganda, Ruto said the eventual establishment of processing plants in Uganda had ended up benefiting both countries by reducing the cost of steel imports within the region.

Both leaders warned against excessive dependence on foreign financing, arguing that outside investors often prioritise access to Africa’s raw materials over the continent’s industrial development goals. Ruto stressed that Africa’s ambitions would remain limited if the continent continued relying on external capital to drive its growth agenda.

Museveni, meanwhile, urged African nations to channel local pension funds and domestic capital into infrastructure and industrial development projects rather than investing heavily overseas. Their remarks echoed findings from the Africa Finance Corporation, which estimates that Africa holds more than US$2 trillion in domestic non-bank capital despite continued underinvestment in industries capable of transforming the continent’s resource wealth.

The summit is expected to continue with discussions and investment negotiations centred on infrastructure, transport, finance, and energy projects across Africa.